My Personal Weekly Dynamic Asset Allocations

Suggestions for ETF Allocations to Outperform the 60/40 Portfolio

TRENDING POSTS

April 19, 2024

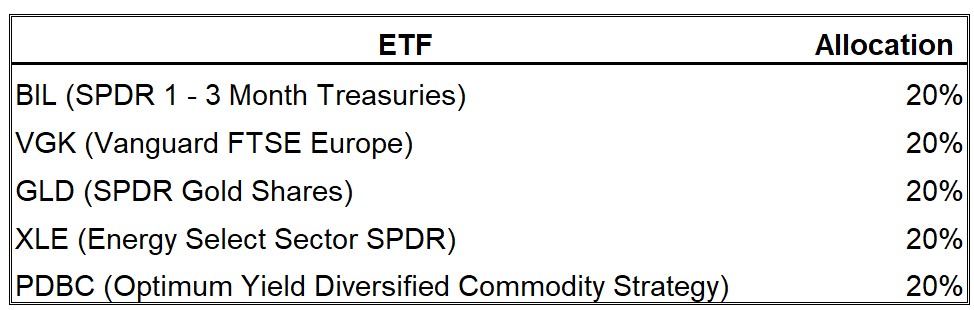

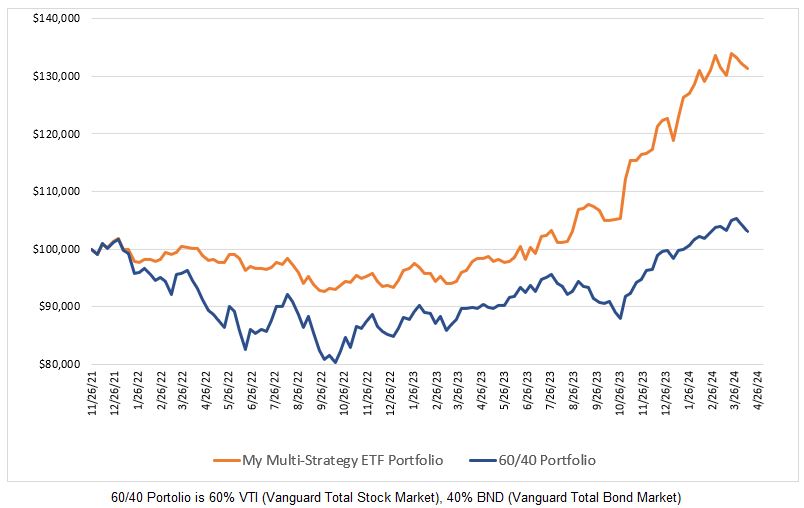

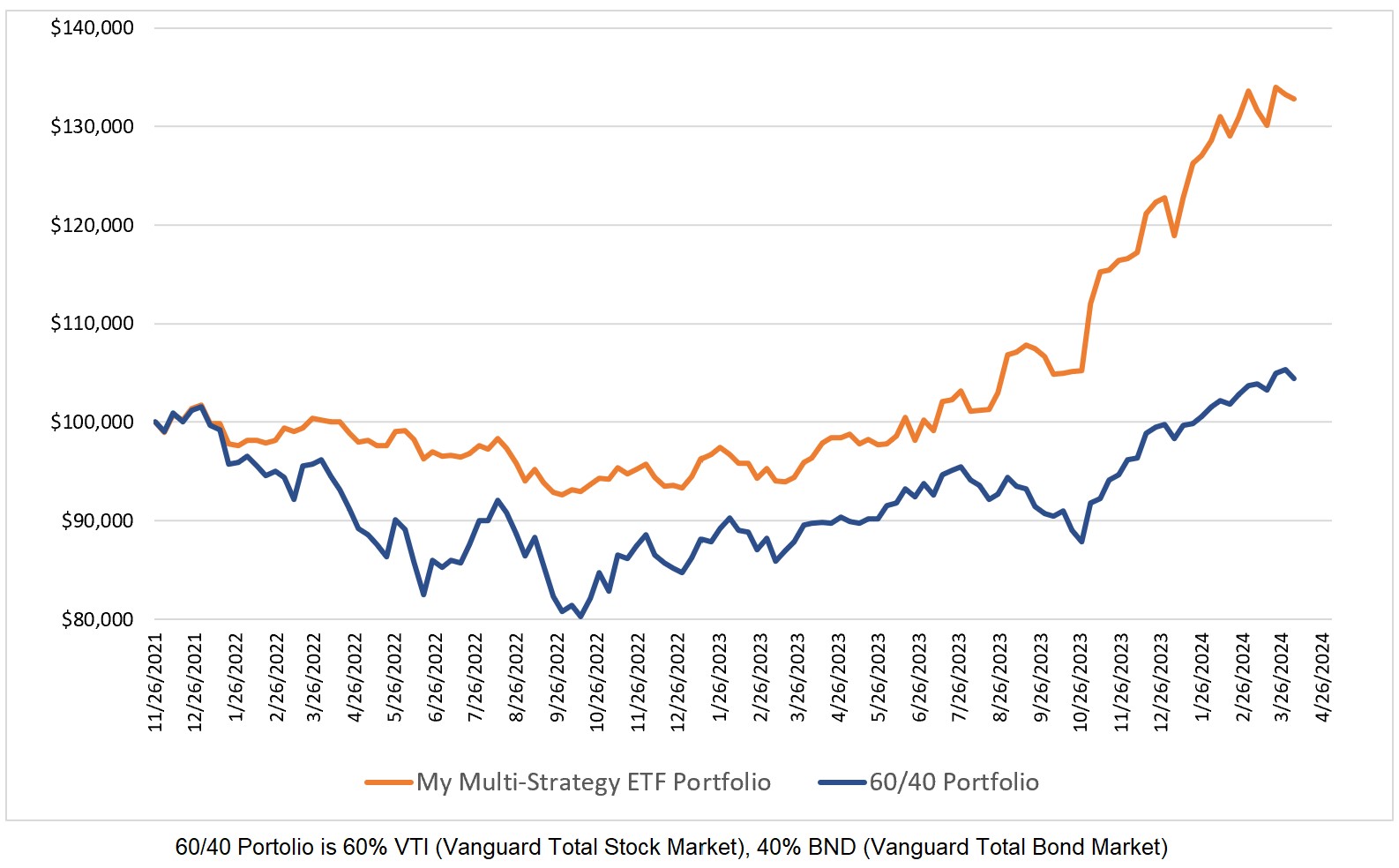

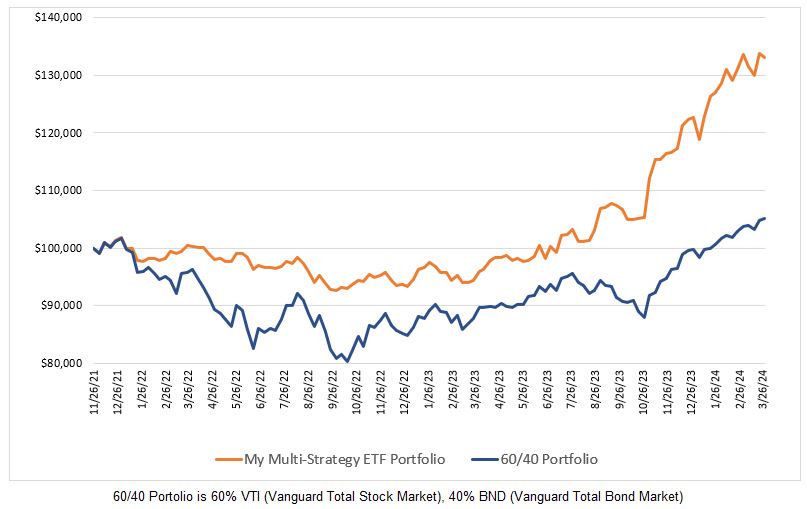

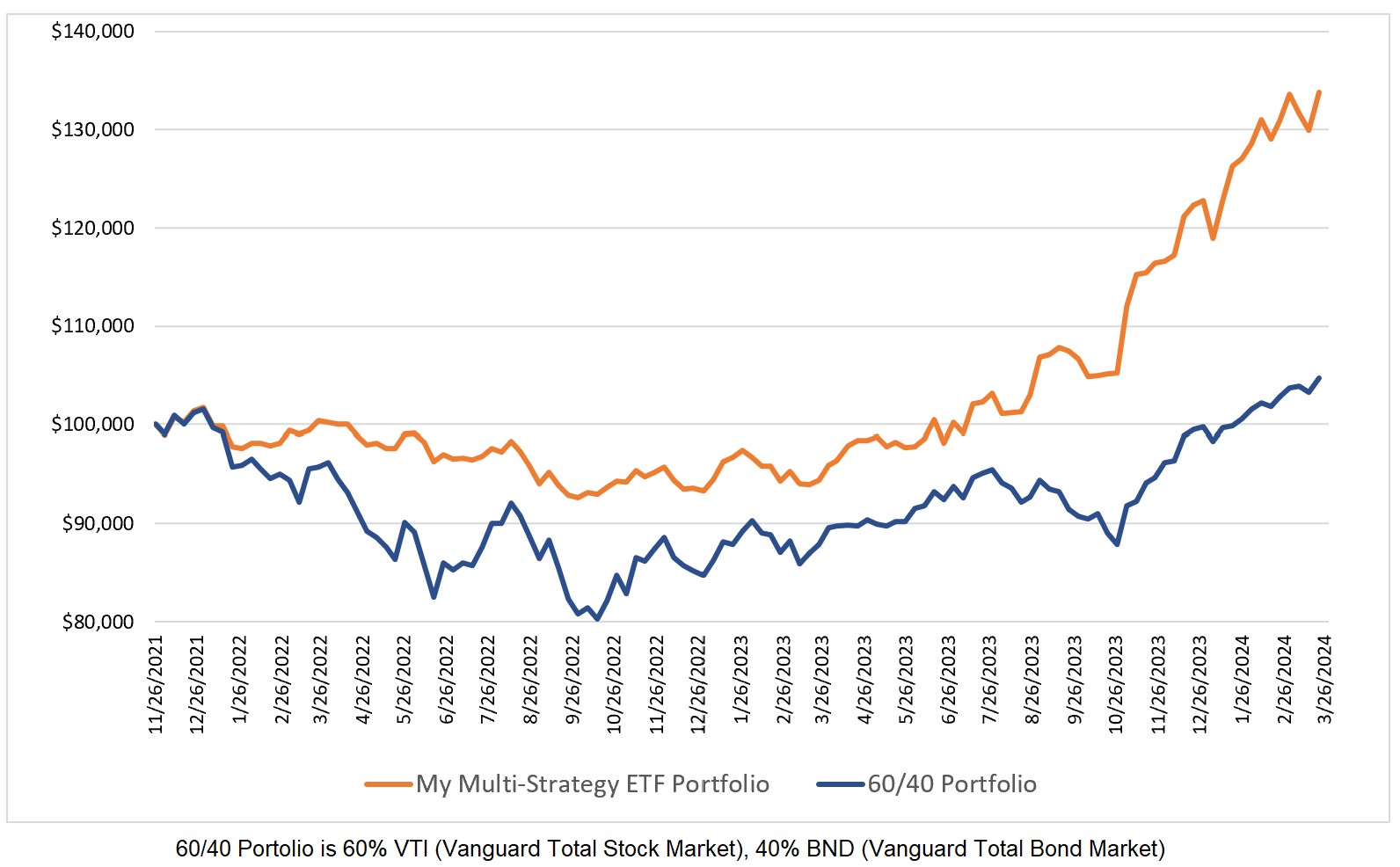

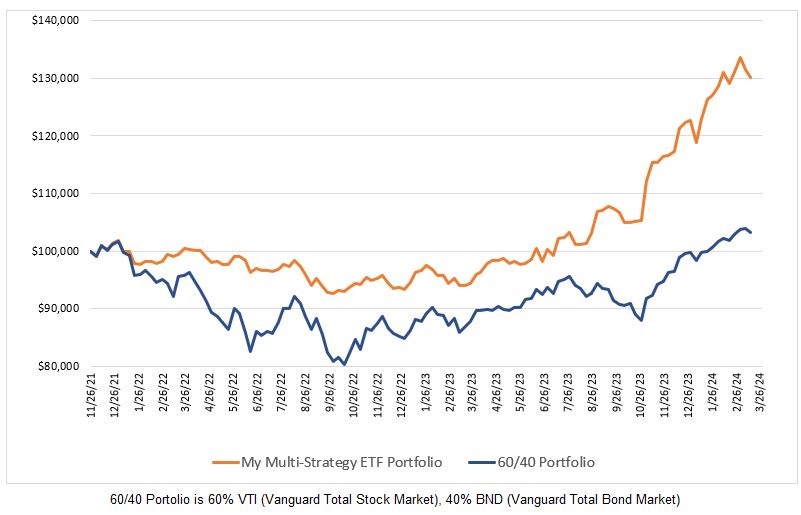

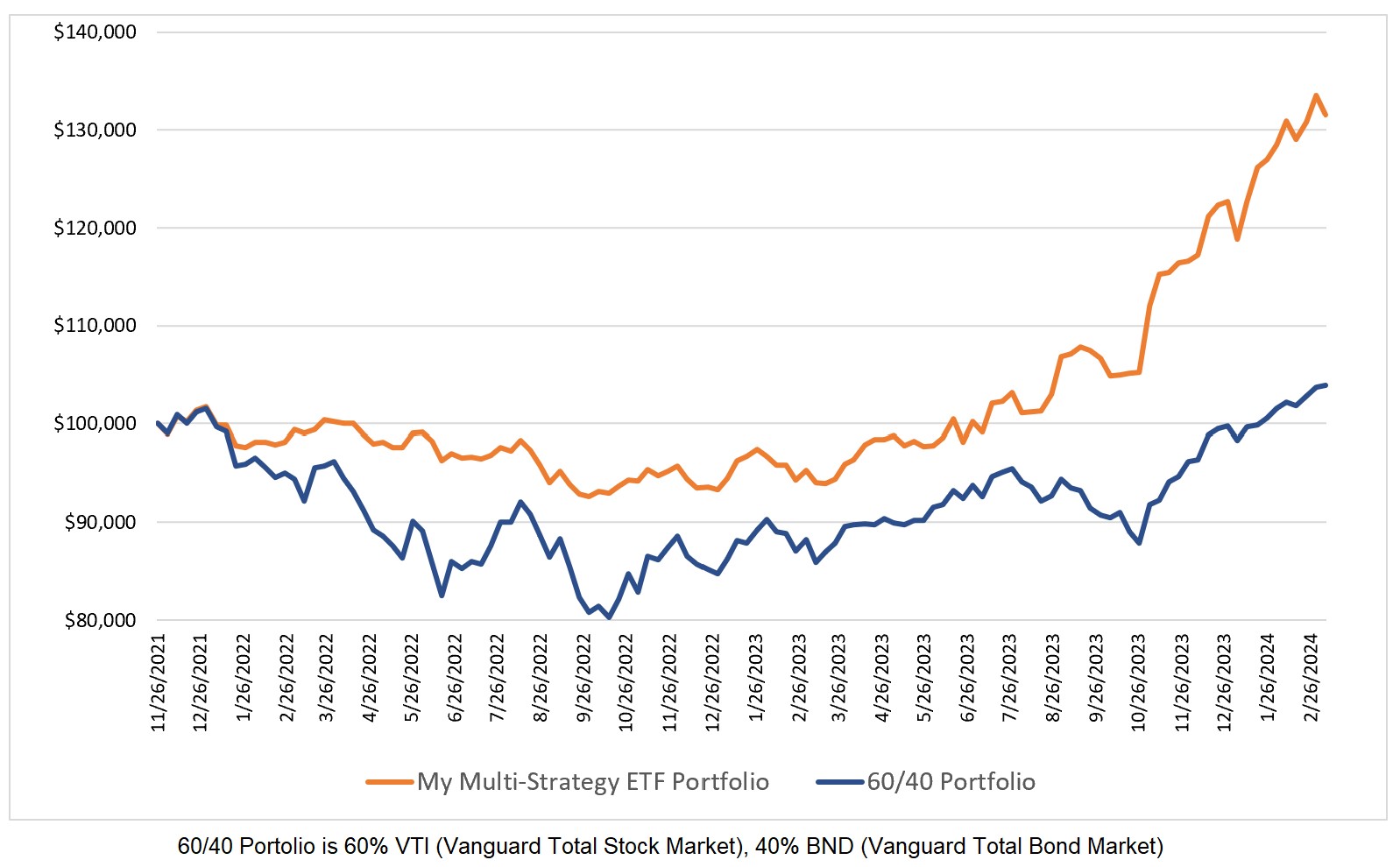

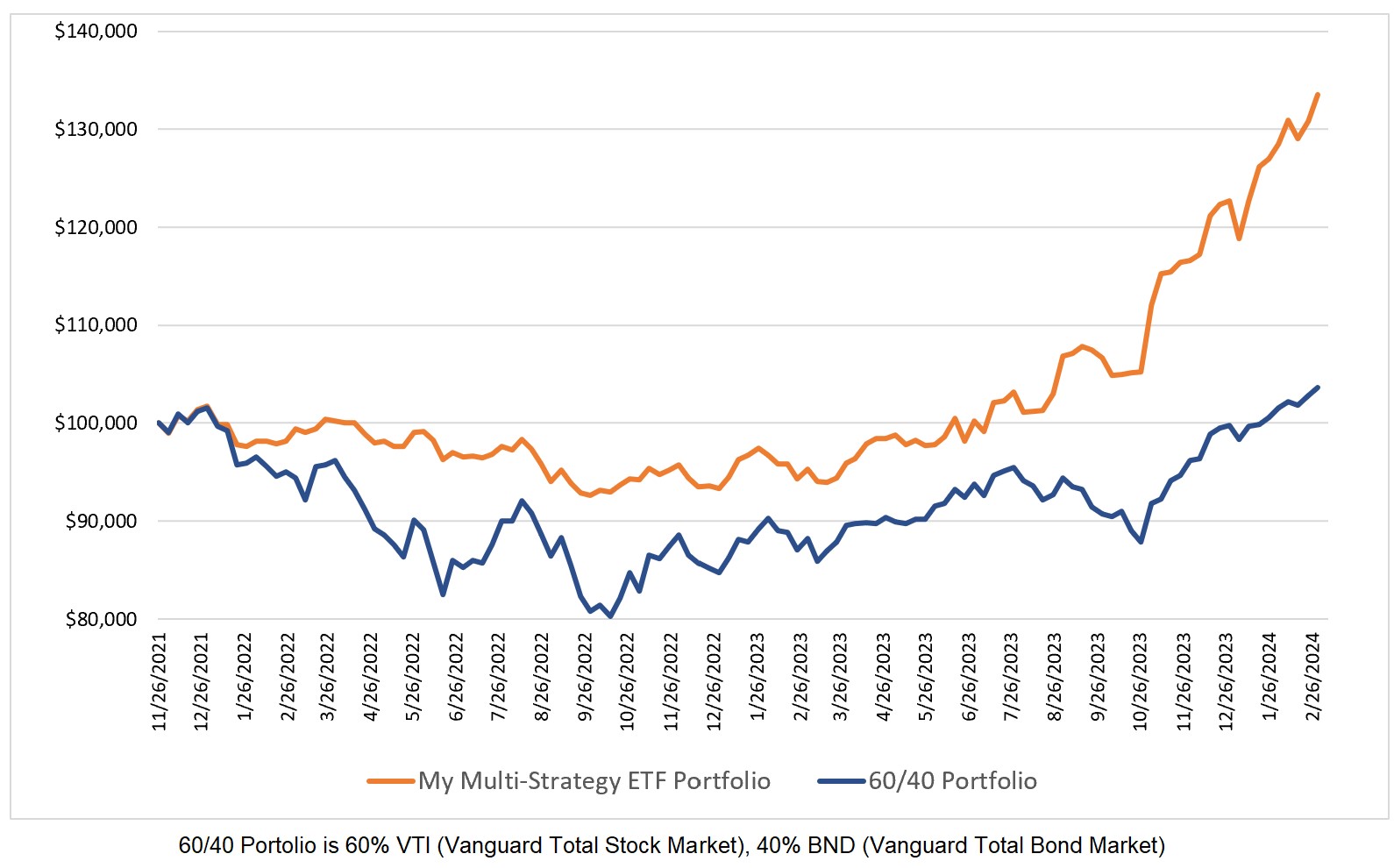

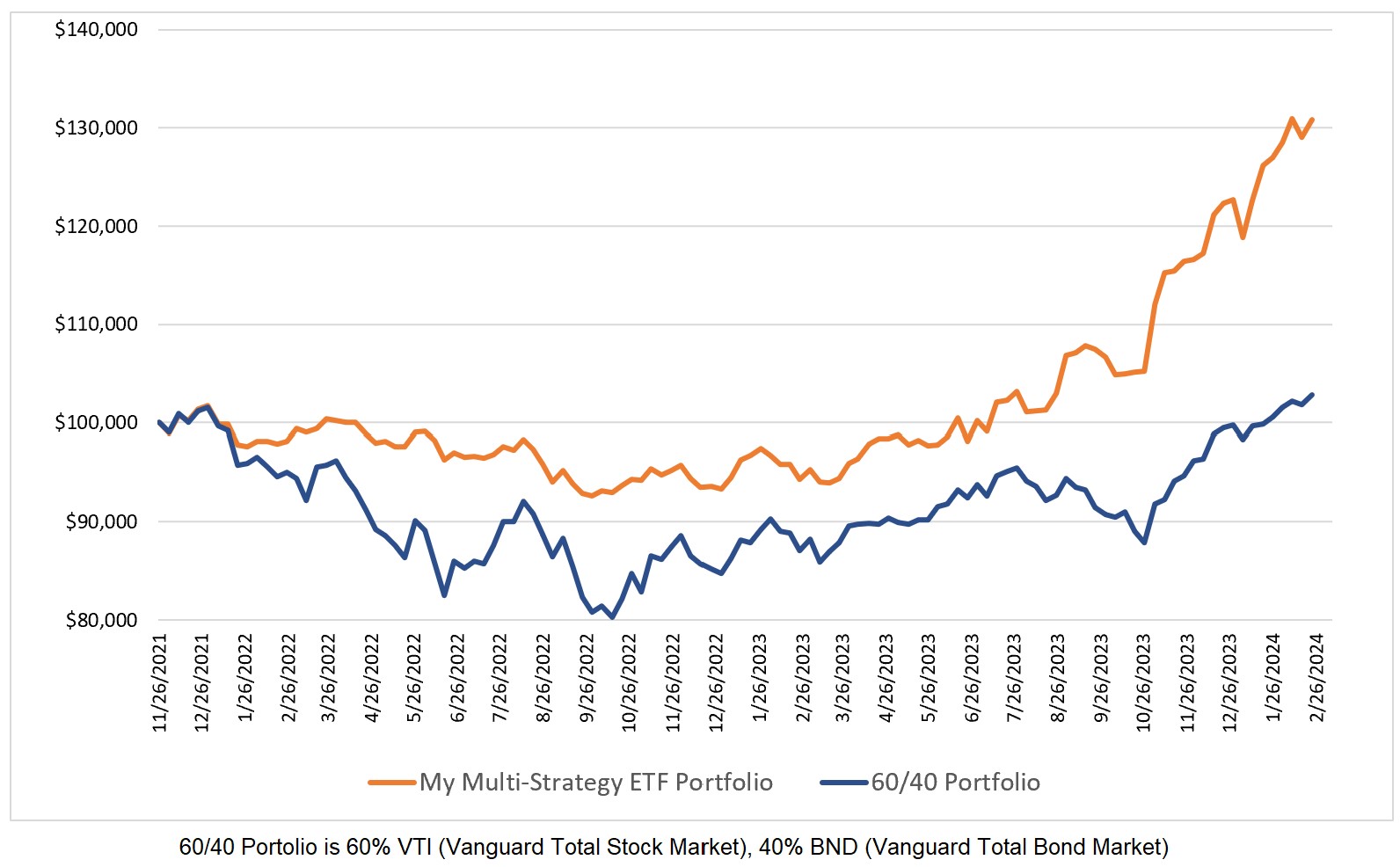

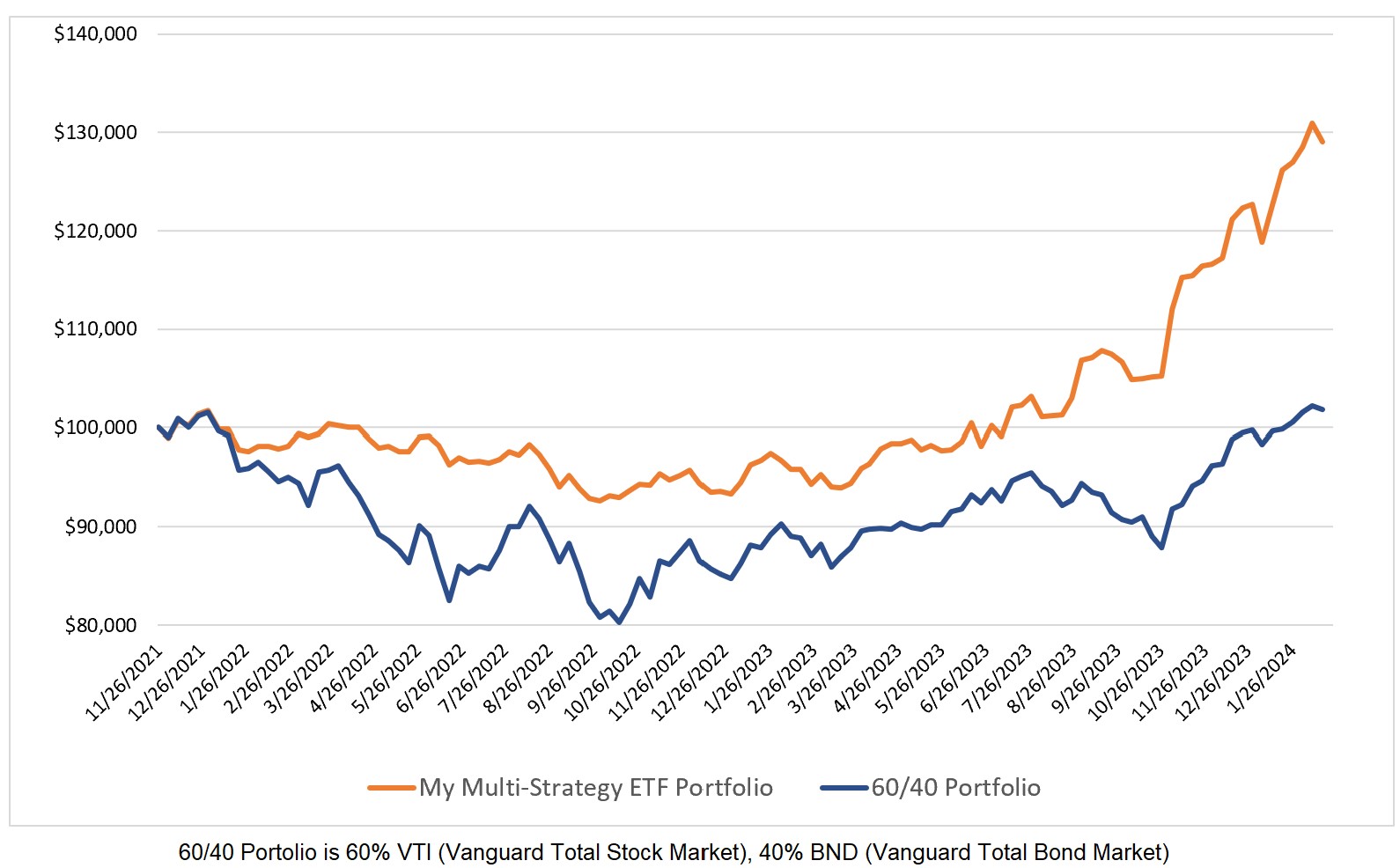

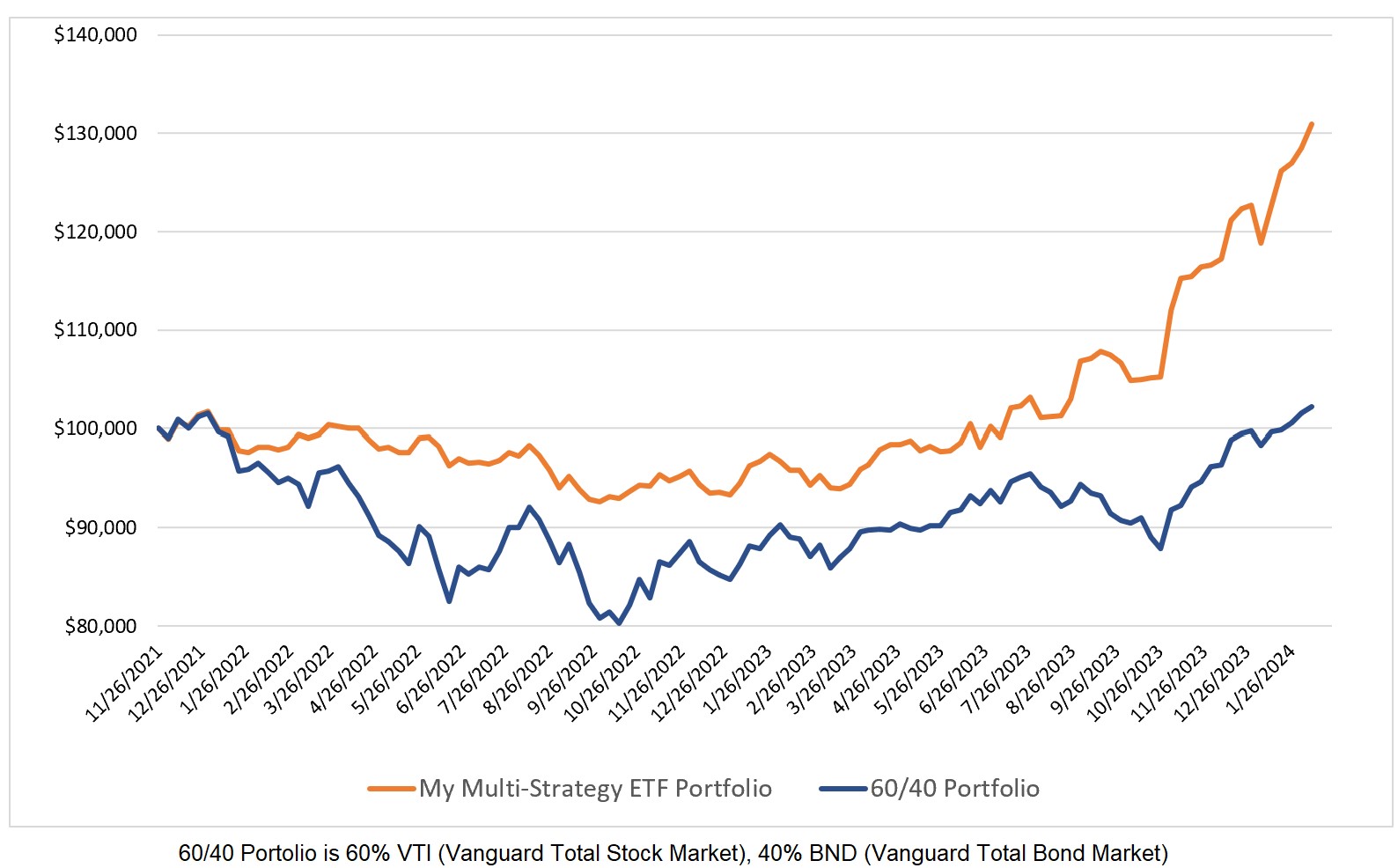

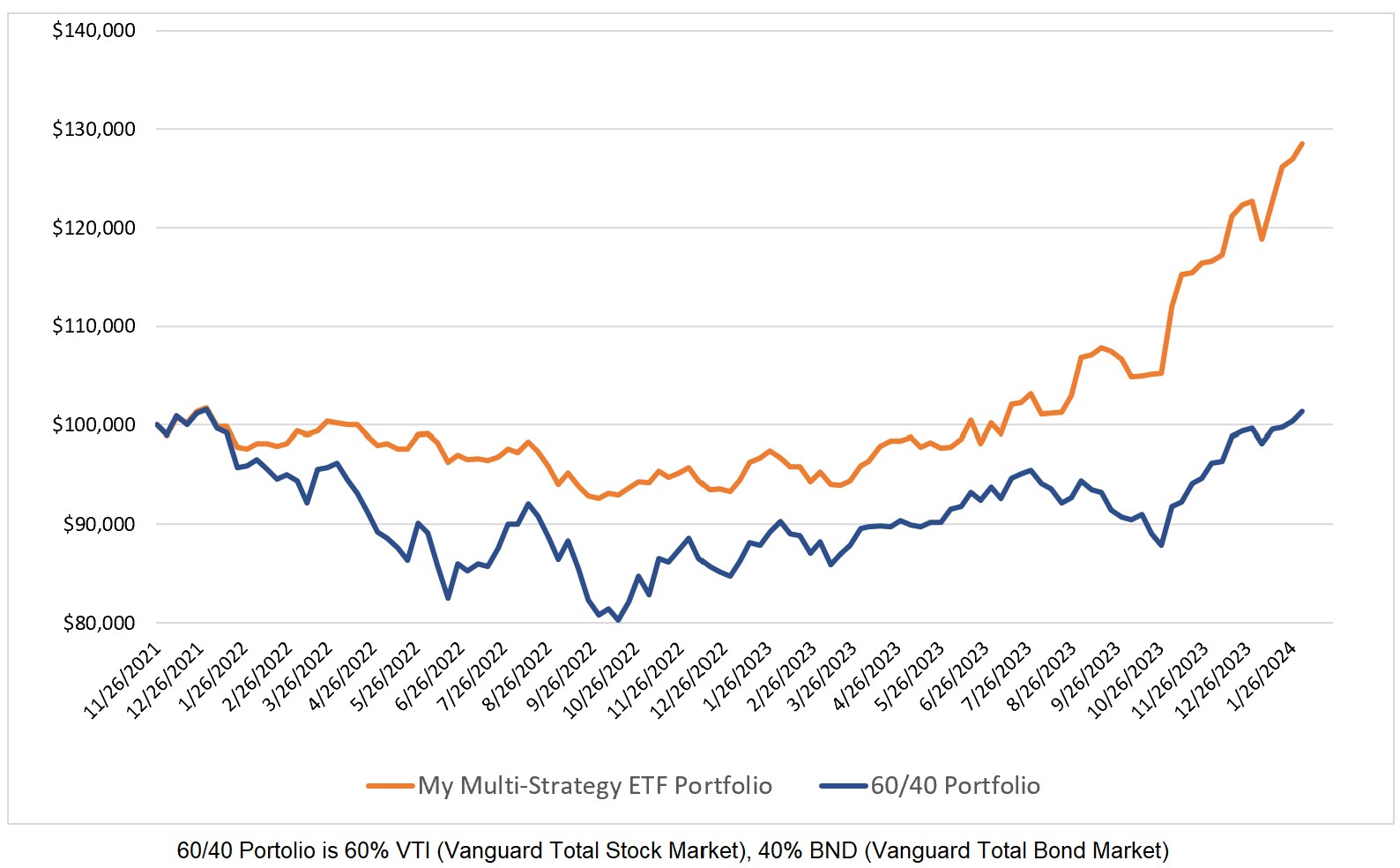

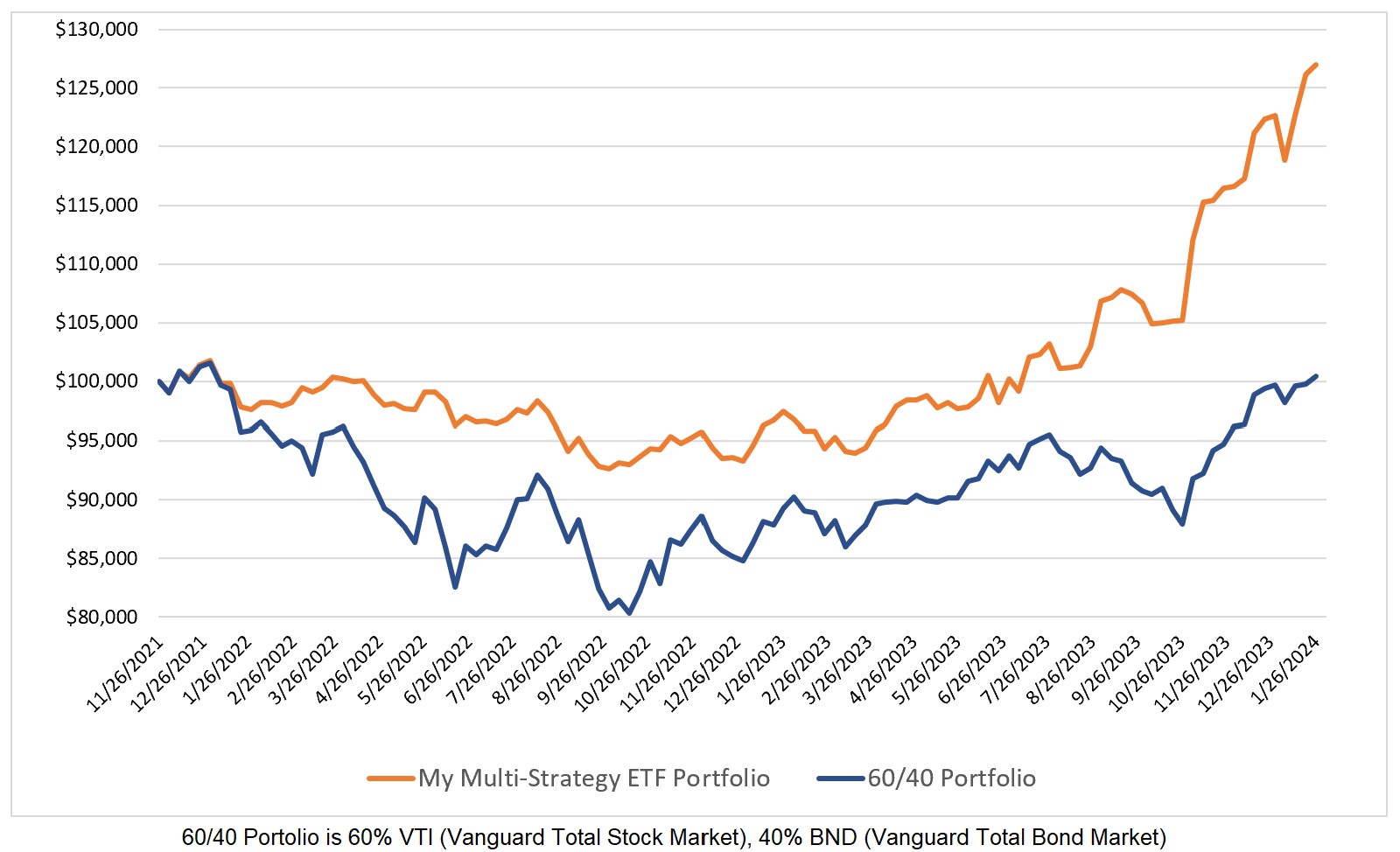

My global multi-strategy ETF model mostly side-stepped an ugly week in the markets as it lost 0.35% compared to a 2.07% loss for the 60/40 model. My model has new...

Read More

Investing Update for the Week Ending April 12, 2024

April 13, 2024

This past week was one in which it was hard to hide from falling prices. Both my Global Multi-Strategy ETF model and the 60/40 fell in price. My model has...

Read More

Investing Update for the Week Ending April 05, 2024

April 5, 2024

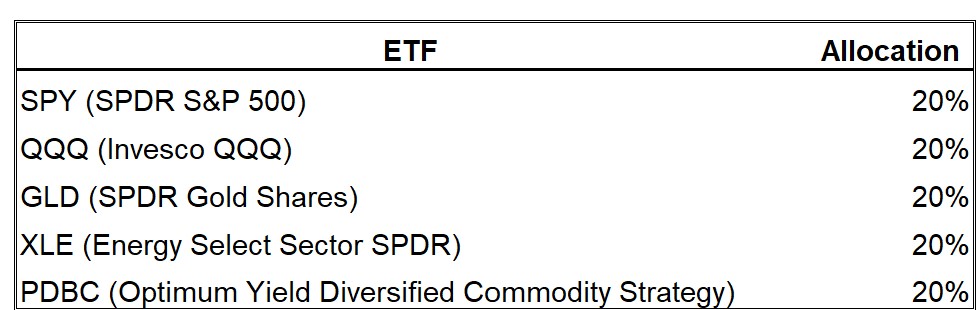

My global multi-strategy ETF model is up 8.2% year-to-date compared to 4.7% for the 60/40 model. The allocation to QQQ only has ended as my model now has allocations to...

Read More

Investing Update for The Week Ending March 29, 2024

March 28, 2024

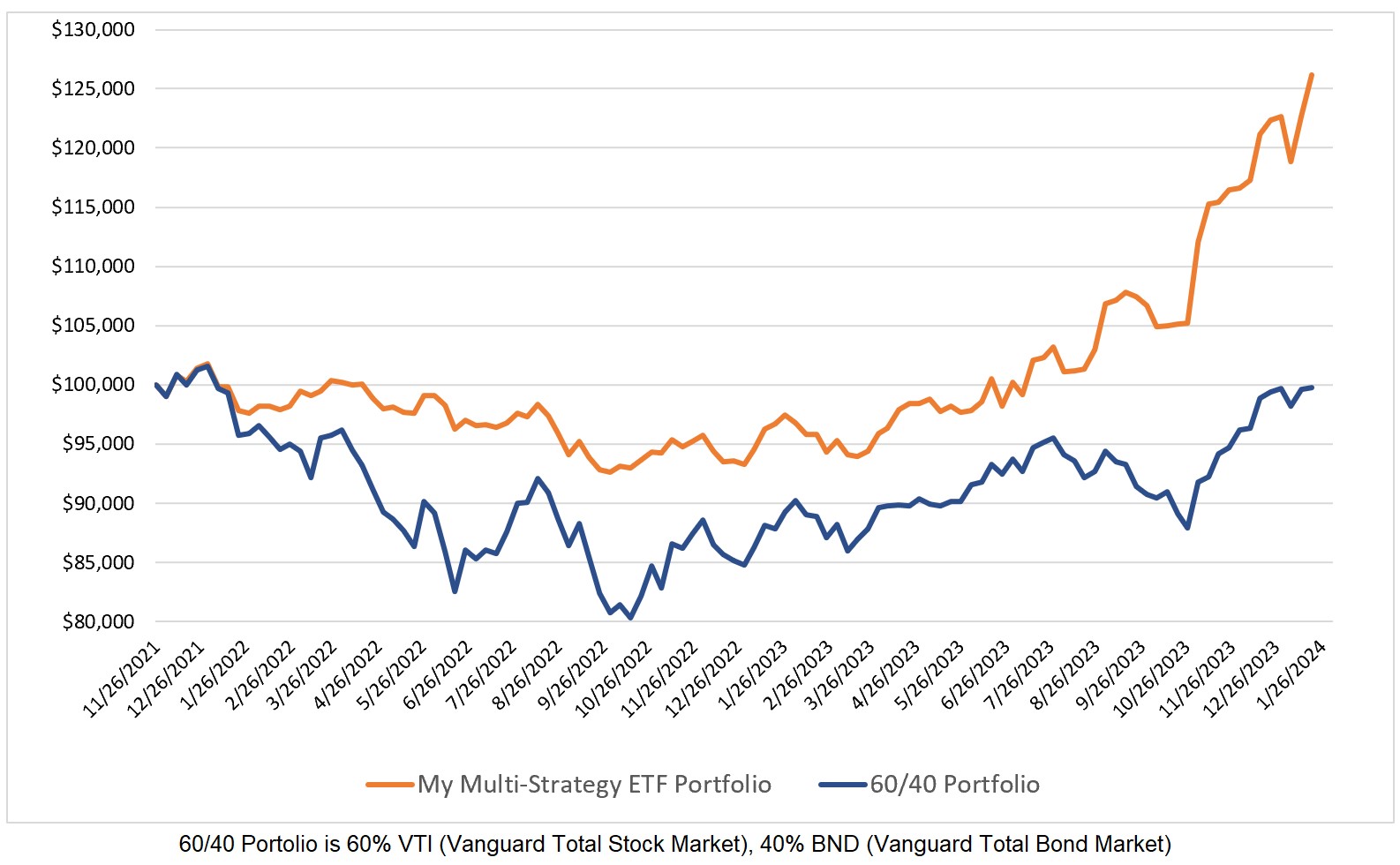

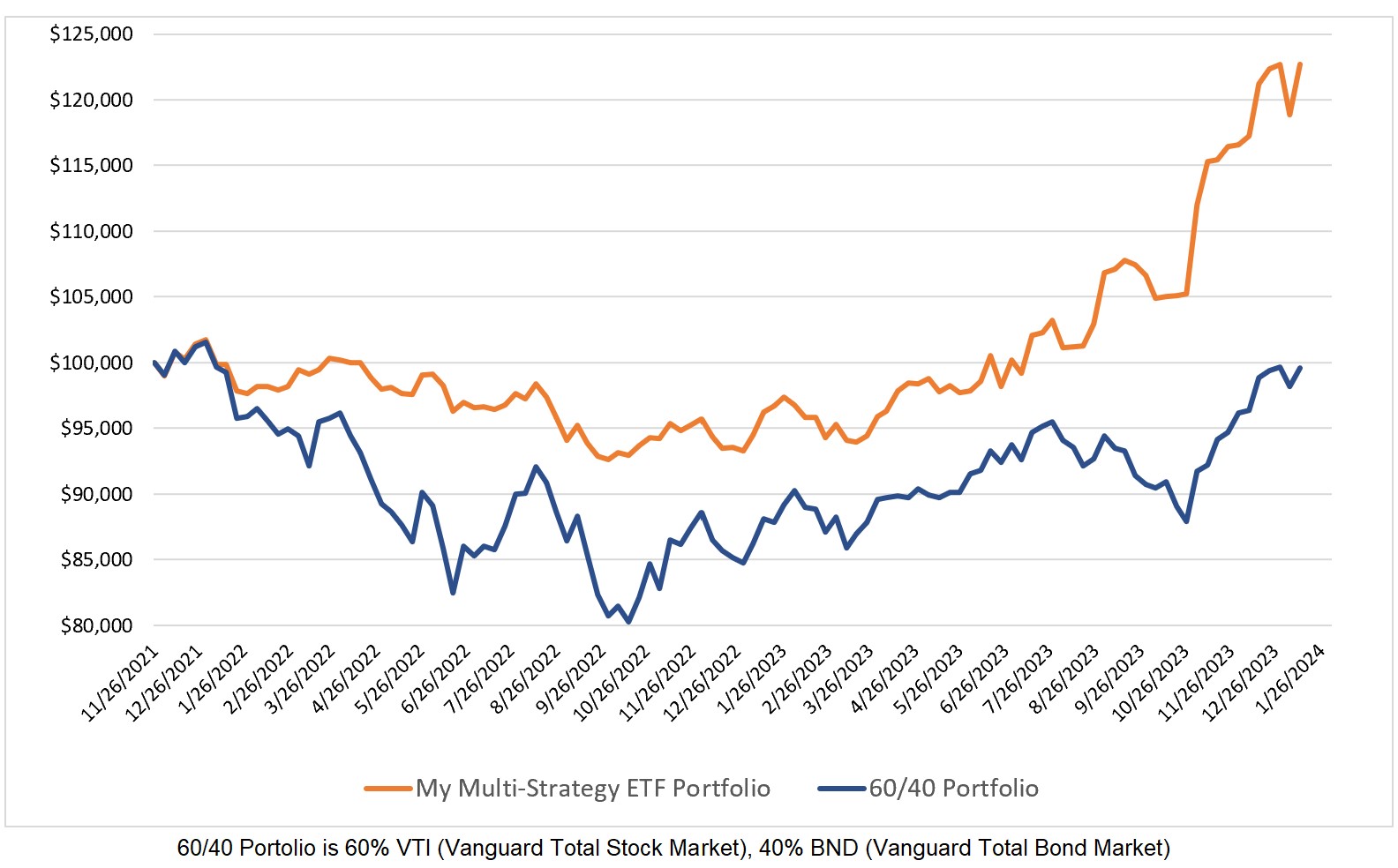

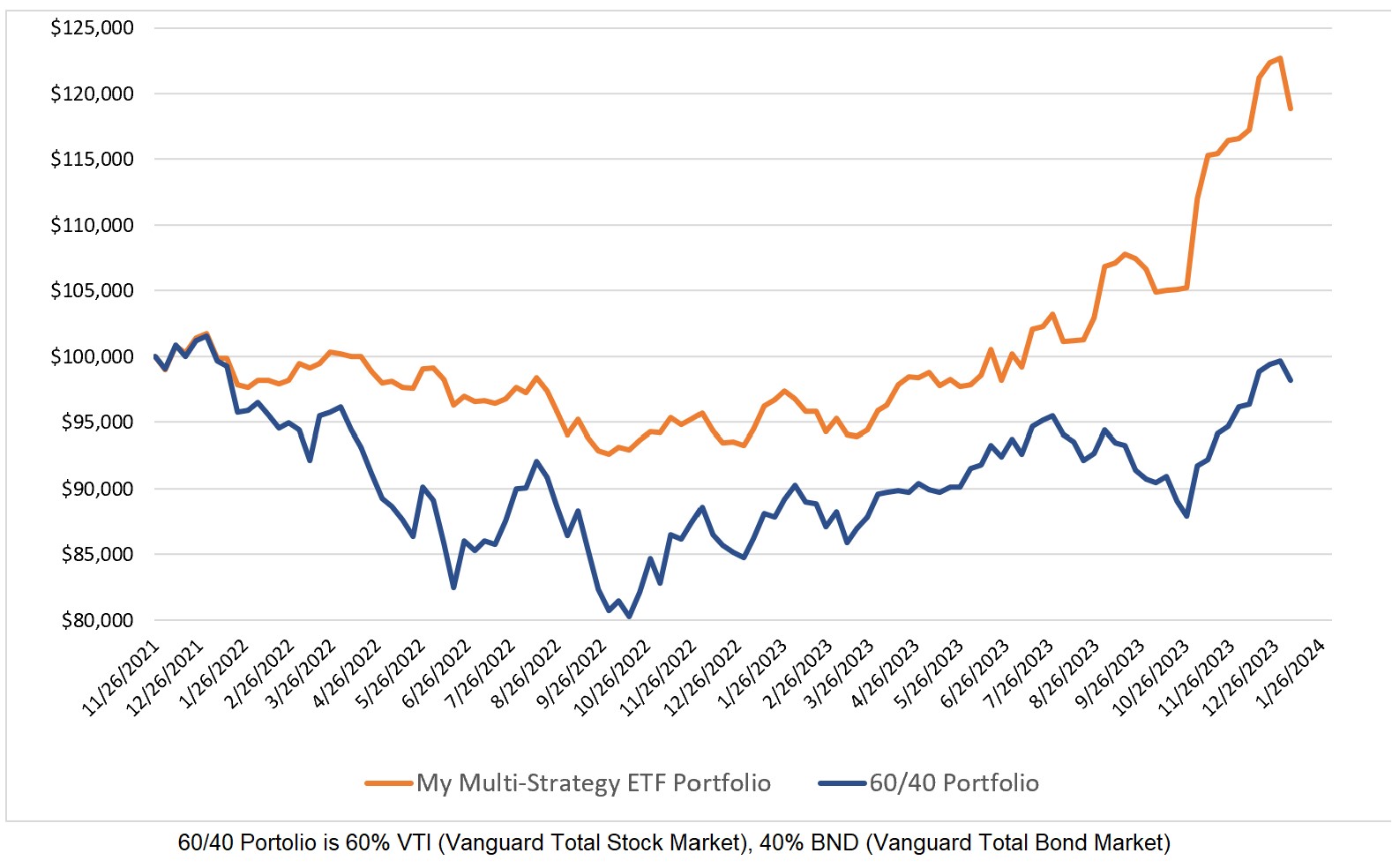

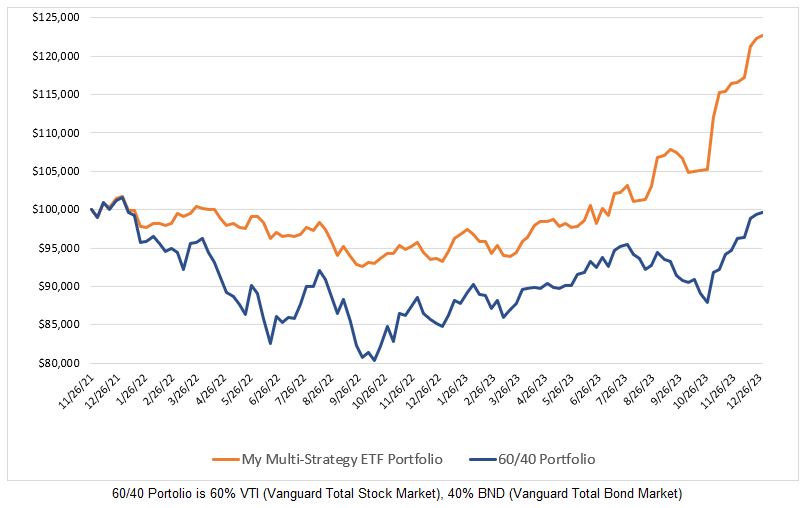

For the twentieth consecutive week, my global multi-strategy ETF model remains 100% allocated to QQQ. My model has increased by 38.8% over the past year compared to a 17.3% increase...

Read More

Investing Update for the Week Ending March 22, 2024

March 22, 2024

My global multi-strategy ETF model rose by 3.01% this past week compared to a 1.43% increase in the 60/40 model. Since I began posting weekly ETF allocation updates here, my...

Read More

Investing Update for the Week Ending March 15, 2024

March 15, 2024

My global multi-strategy ETF model fell by 1.16% this week compared to a 0.63% decline in the 60/40 model. There is no change this week as my model remains 100%...

Read More

Investing Update for the Week Ending March 08, 2024

March 8, 2024

My global multi-strategy ETF model declined by 1.48% compared to a 0.19% gain for the 60/40 model this week. For the seventeenth consecutive week, my model remains 100% allocated to...

Read More

Investing Update for the Week Ending March 01, 2024

March 2, 2024

It was another positive week for my global multi-strategy ETF model as it rose by 2.02% compared to an increase of 0.77% for the 60/40 (VTI/BND) model. Since I began...

Read More

Investing Update for the Week Ending February 23, 2024

February 23, 2024

It was a positive week as my global multi-strategy ETF model rose by 1.44% vs 0.95% for the 60/40 model. There is no change in the allocation as my model...

Read More

Investing Update for the Week Ending February 16, 2024

February 16, 2024

My global ETF multi-strategy model declined by 1.48% this past week compared to a 0.31% loss for the 60/40 model. Over the past year, my model has generated a 34.6%...

Read More

Investing Update for the Week Ending February 09, 2024

February 9, 2024

What I am about to say, you have heard over and over for the past three months. My global multi-strategy ETF model was up this week and remains 100% allocated...

Read More

Investing Update for the Week Ending February 02, 2024

February 2, 2024

Eventually, the trend will bend and end. Until then, it's your friend. It was another positive week for my multi-strategy global ETF model as it rose by 1.23% compared to...

Read More

Investing Update for the Week Ending January 26, 2024

January 26, 2024

My multi-strategy global ETF model rose by 0.62% this week vs 0.66% for the 60/40. For the eleventh consecutive week, my model remains 100% invested in QQQ.

Read More

Investing Update for the Week Ending January 19, 2024

January 19, 2024

It was another great week for my global ETF multi-strategy model as it gained 2.84% versus a 0.18% gain for the 60/40 model. For the 10th consecutive week, my model...

Read More

Investing Update for the Week Ending January 12, 2024

January 12, 2024

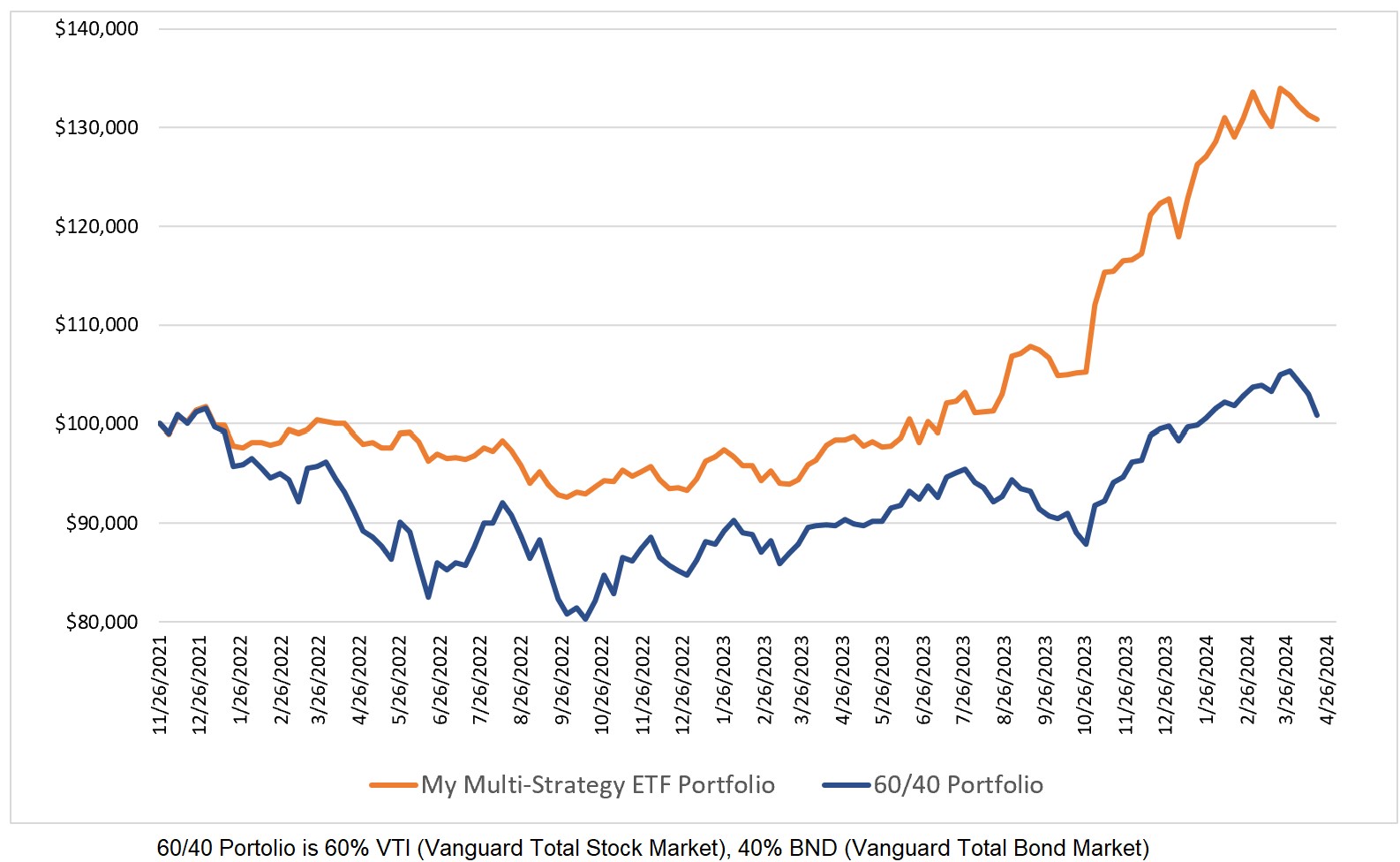

Last week's decline was followed by this week's bounce. Since I began posting weekly ETF allocations here on this site in November 2021, my multi-strategy ETF model has outperformed the...

Read More

Investing Update for the Week Ending January 05, 2024

January 5, 2024

Happy New Year and may 2024 bring you health and prosperity. My multi-strategy ETF model fell by 3.11% this week versus a 1.47% drop in the 60/40. There is no...

Read More

Investing Update for the Week Ending December 29, 2023

December 29, 2023

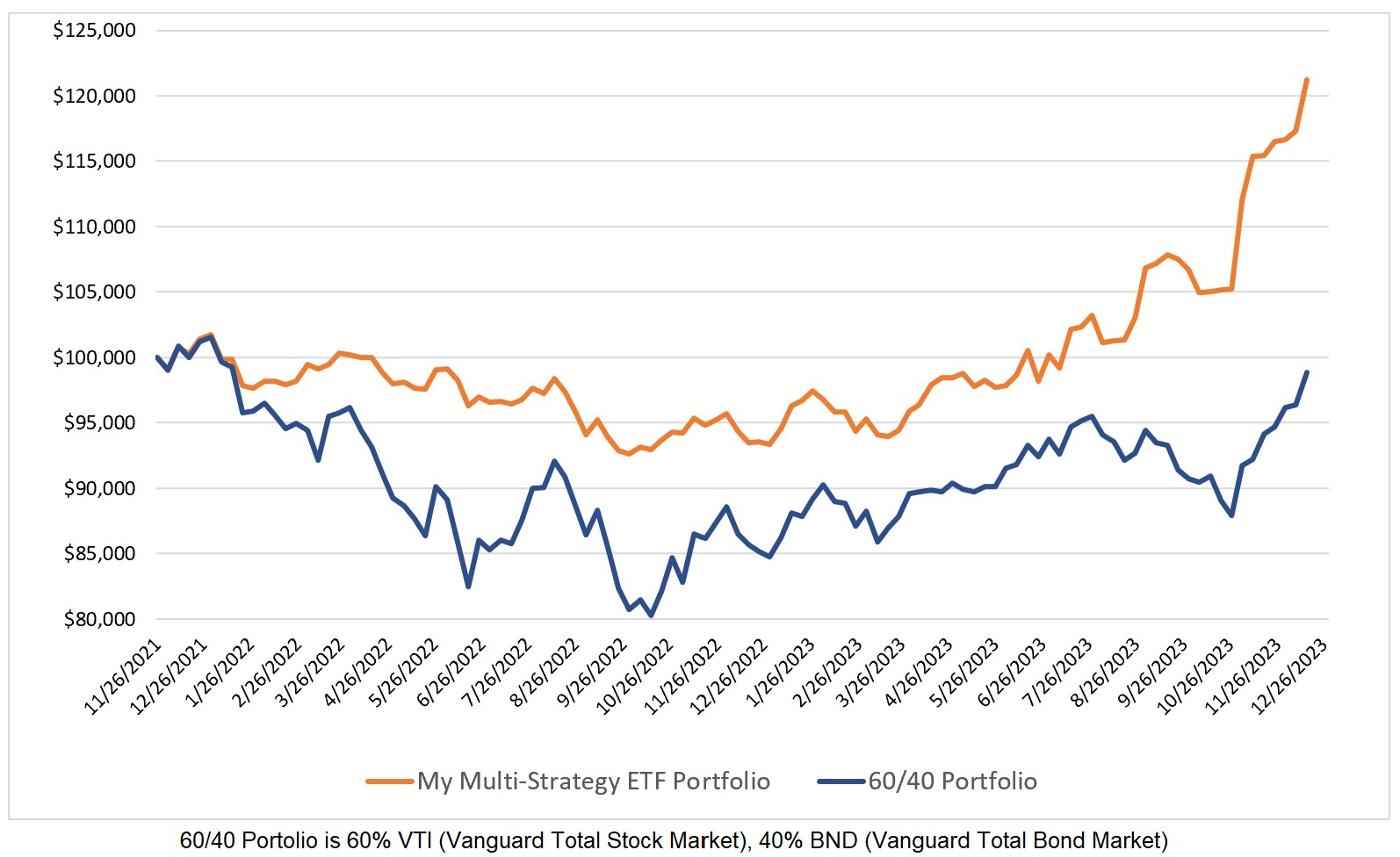

With a small gain in the final week of trading for 2023, my multi-strategy ETF model finished the year with a 31.5% gain versus a 17.6% gain for the 60/40....

Read More

Investing Update for the Week Ending December 15, 2023

December 15, 2023

This was a great week as far as investing goes. My model portfolio was up 3.36% and the 60/40 model was up 2.58%. My model now has a CAGR that...

Read More

Investing Update for the Week Ending December 08, 2023

December 8, 2023

With a 0.57% gain this week, my multi-strategy ETF model is up 25.7% year-to-date versus 13.6% for the 60/40 model. There is no change in the allocation of my model...

Read More

Investing Update for the Week Ending December 01, 2023

December 1, 2023

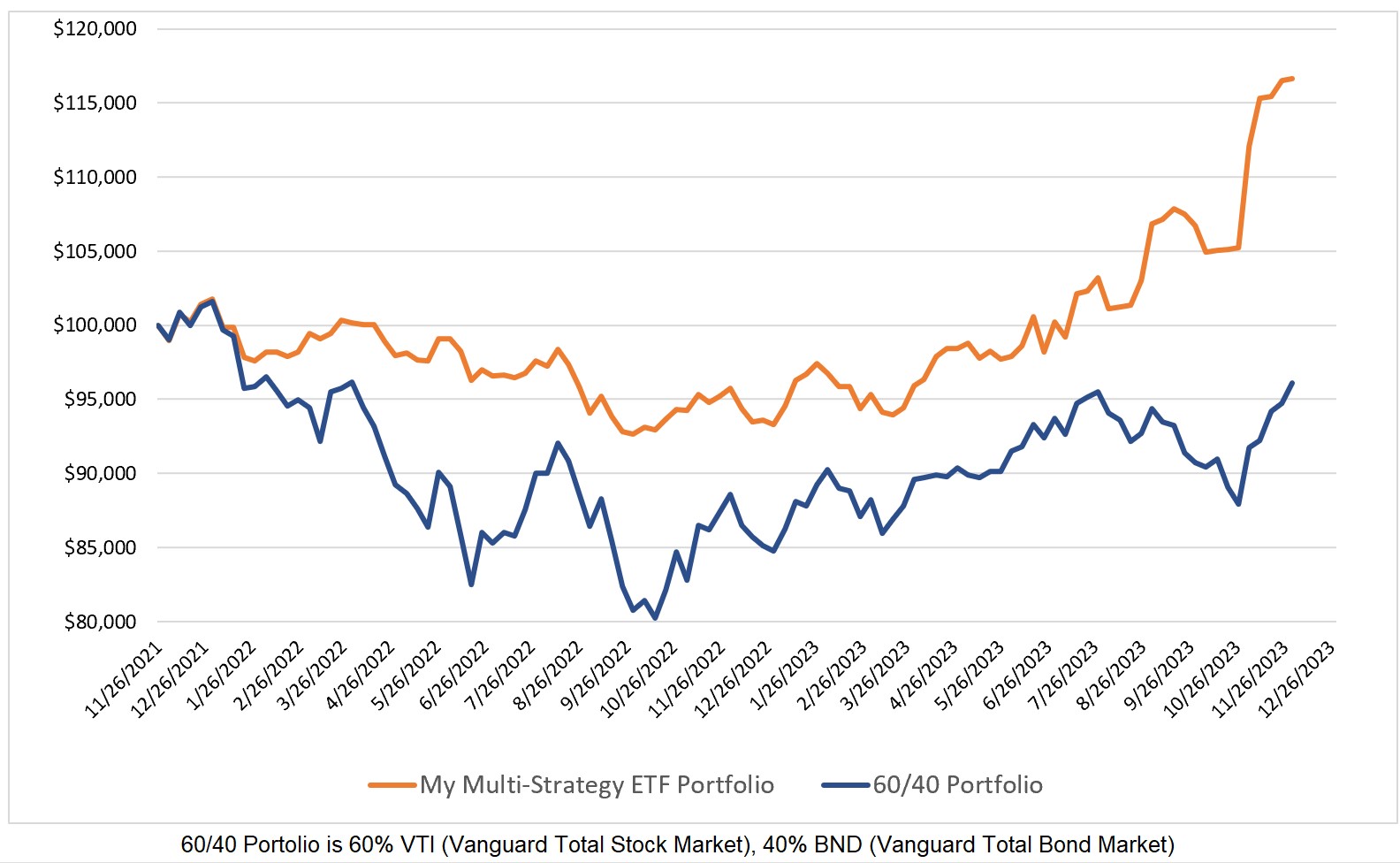

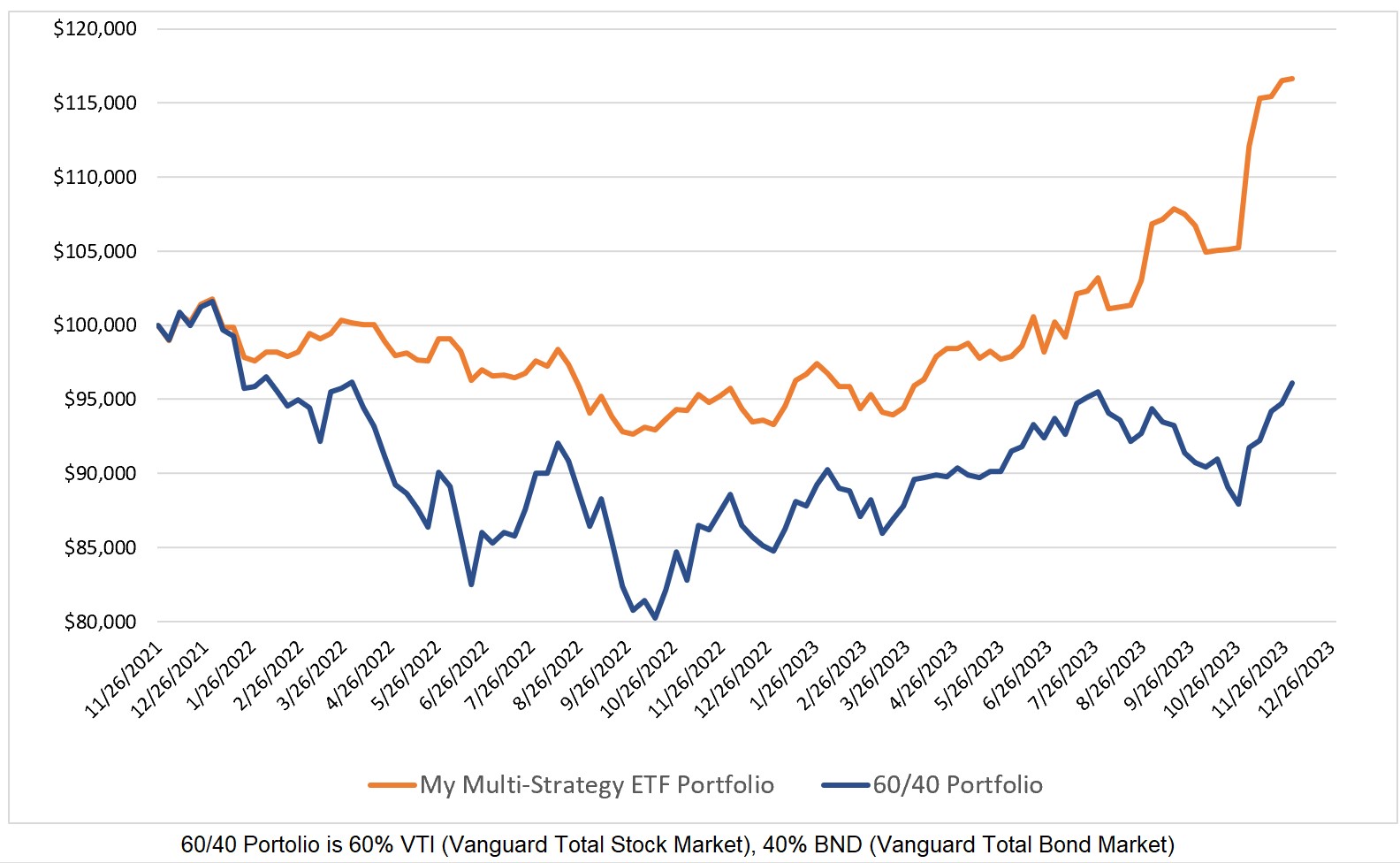

The 60/40 model won the race this week with a 1.45% gain compared to a 0.11% gain for my multi-strategy ETF model. With a CAGR that is 9.9% higher and...

Read More

Disclaimer:

The Systematic Trader. This site may include market analysis. All ideas, opinions, and/or forecasts, expressed or implied herein, are for informational purposes only and should not be construed as a recommendation to invest, trade, and/or speculate in the markets. Any investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied herein, are committed at your own risk, financial or otherwise. © 2023